Business Accounting for Business Assignment Sample

Get expert insights into accounting for business with Rapid Assignment Help, covering key financial strategies, investment appraisals, and cost optimization techniques.

- 1: Investment Appraisal Overview in BA Business Accounting

- 2: Analysis of Investment Appraisal Techniques in Business Accounting

- 2.1: Usefulness

- 2.2: Limitations

- 3: Practical Application and Deployment

- 3.1: Recommendation for selection

- 3.2: Potential resolutions for mitigating conflict of NPV and IRR

- 3.3: Impacts of cost of capital on the net present value of each project

- Type Assignment

- Downloads6051

- Pages5

- Words1196

1: Investment Appraisal Overview in BA Business Accounting

This assignment will cover important attributes of accounting applicable for business where investment appraisal techniques and their associated viability will be illustrated. Fundamental priority of this assignment will be offered for evaluating usefulness and limitations of various investment appraisal methods while plausible recommendations for selection of a project will be offered subsequently. Analysis of potential resolutions for mitigating conflicts of NPV and IRR will be subsequently discovered in this assignment while impacts of cost of capital on net present value of each project will be detected in brief.

2: Analysis of Investment Appraisal Techniques in Business Accounting

2.1: Usefulness

Accounting Rate of Return

The usefulness of “accounting rate of return” mainly consists of being an easy calculative method for determining percentile returns that can be fetched if an investment is undertaken by a company. As viewed by Magni and Marchioni (2020), additional advantages of the “accounting rate of return” method also involves facilitation of easy investment decision making frameworks since complexities associated are minimal with this method.

Payback Period

Usefulness of the payback period method fundamentally involves allowing organisations the ability to detect the overall duration needed for an investment to recover its initial investment costs with available cash flows. Additional usefulness of the “payback period” method involves its calculative feature where the method is usually easier to be applied.

Net Present Value

Usefulness of the “net present value” mainly include application of time value of money for determining discounting values of cash flow and to obtain expected returns that can be generated from an investment in currencies. As per explanations of Siziba and Hall (2021), usefulness of “net present value” also includes the method being the most plausible tool for investment decision making thereby allowing sensible and judicious decision-making facilities initiated by organisations.

Get assistance from our PROFESSIONAL ASSIGNMENT WRITERS to receive 100% assured AI-free and high-quality documents on time, ensuring an A+ grade in all subjects.

Internal Rate of Return

Usefulness of the “internal rate of return” method fundamentally involves consideration to percentile value of expected future returns that can be generated from an investment proposal. Additional usefulness of “internal rate of return” method also involves comparative characteristics where a project feasibility can be compared with cost of capital to decide selection or rejection of a specific investment project.

2.2: Limitations

Accounting Rate of Return

Fundamental limitations of the “accounting rate of return” method involves lack of consideration for future risks since this method follows a symmetric and linear profitability approach. Additional demerits of this method involve exclusion of time value of money consideration where effects of economic influences cannot be evaluated.

Payback Period

The “payback period” method contains the primary limitation of not addressing percentile or monetary returns that can be obtained by an organisation when an investment appraisal is undertaken. Saługa et al. (2021), critically stated that disadvantages of “payback period” method also include exclusion of discounting applications where cash flows evaluated are primarily non-discounted.

Net Present Value

Limitations of the “net present value” method are mainly associated with uncertainties pertaining to discounting rate and other economic factors. Wang and Lee (2021), critically opined that the NPV method of investment appraisal is also limited with providing currency-based returns and assessment of percentile returns cannot be fetched in this method.

Internal Rate of Return

Limitations of the internal rate of return method mainly involve non-consideration of time value of money thereby excluding discounting applications for cash flows. As Alkaraan (2020), critically narrated those additional limitations of the “internal rate of return” method include lack of offering currency-based returns since percentage values are only obtained in this method.

3: Practical Application and Deployment

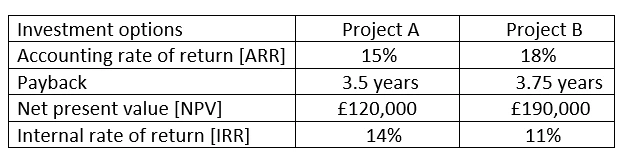

3.1: Recommendation for selection

The above figure expresses superior “payback” and “internal rate of return” achieved by project A, while “net present value” and “accounting rate of return” for project B is deemed superior. The project selection criteria applicable for the company emphasises payback period method as the primary tool and hence project A should be chosen.

3.2: Potential resolutions for mitigating conflict of NPV and IRR

In order to mitigate conflict associated with project preferences based on differentiated NPV and IRR for project A and project B, primary emphasis is needed to be offered towards assessment of project selection criteria followed. The company mainly follows the project selection criteria of lower payback period in which project A contains a marginally better payback than project B. Based on this criterion, project A should be selected by the company since this project meets necessary criteria’s applicable for selection. Shaturaev (2023), stated that when project duration for available options is similar then potential resolutions for mitigating conflict between NPV and IRR should be met by prioritising “net present value” over “internal rate of return”. This is mainly followed since higher NPV of a project is deemed more feasible and allows a company the scope to maximise financial returns that can be obtained. Based on NPV priority, project B should be chosen by the company since it fetches a higher financial return as opposed to project A.

3.3: Impacts of cost of capital on the net present value of each project

The impact of cost of capital on “net present value” of each project is mostly considered to contain an inverse relationship. As part of the inverse relationship, an increase in cost of capital is likely to decrease the “net present value” while a decrease in the cost of capital for each project is likely to raise “net present value”.

Conclusion

This assignment has discovered that project A should be chosen due to a relatively lower payback period achieved in comparison to project B. Limitations of investment appraisal techniques have also been conducted in this assignment where payback period and accounting rate of return are limited concerning application of time value of money, often clarified through Assignment Help Online, “Net present value” method and internal rate of return method are considered to be beneficial since accurate estimation of percentile and monetary returns can be detected.

Recommendations

Recommendations that additionally offered involve consideration to identify cost optimisation techniques if project A is to be undertaken. Application of cost optimisation techniques will offer the company scope to increase its profitability that can make the new investment highly attractive in financial terms.

Reference List

- Alkaraan, F., 2020. Strategic investment decision-making practices in large manufacturing companies: a role for emergent analysis techniques?. Meditari accountancy research, 28(4), pp.633-653.

- Magni, C.A. and Marchioni, A., 2020. Average rates of return, working capital, and NPV-consistency in project appraisal: A sensitivity analysis approach. International Journal of Production Economics, 229, p.107769.

- Saługa, P.W., Zamasz, K., Dacko-Pikiewicz, Z., Szczepańska-Woszczyna, K. and Malec, M., 2021. Risk-adjusted discount rate and its components for onshore wind farms at the feasibility stage. Energies, 14(20), p.6840.

- Shaturaev, J., 2023. Efficiency of investment project evaluation in the development of innovative industrial activities. ASEAN Journal of Science and Engineering, 3(2), pp.147-162.

- Siziba, S. and Hall, J.H., 2021. The evolution of the application of capital budgeting techniques in enterprises. Global finance journal, 47, p.100504.

- Wang, S.Y. and Lee, C.F., 2021. A fuzzy real option valuation approach to capital budgeting under uncertainty environment. In Encyclopedia of Finance (pp. 1-24). Cham: Springer International Publishing.

Recently Downloaded Samples by Customers

Introduction Enhance your academic success with Assignment Help UK, emphasizing the importance of time management,...View and Download

Introduction to Minimise Sedative Drugs Used On Patients Assignment Sample Background Information Sleep is one of the basic...View and Download

Chapter 1: Introduction Get free samples written by our Top-Notch subject experts for taking online Assignment Helper...View and Download

Introduction - BU7044 Corporate Governance and Ethics Corporate governance and ethics are a set of processes and principles...View and Download

Part A: Key Reasons Behind the Failure of the Metaverse Project The failure of the Metaverse project can be attributed to...View and Download

Introduction to Auditing Assignment Sample Audit Senior 1 Company background Compass Group plc. is a British multinational...View and Download